How to Get a Primary Care Doctor With Insurance: A Complete 2026 Guide

Last updated: May 28, 2026

Quick Answer: To get a primary care doctor with insurance, call your insurer to get a list of in-network physicians, confirm the doctor is accepting new patients, then schedule a new patient appointment with your insurance card and ID ready. The process typically takes one to four weeks from search to first visit, though practices like IDCC Health Services in Brooklyn offer same-day appointments that can shorten that timeline significantly.

Trust family doctor in Brooklyn Experts

Key Takeaways

- Always verify a doctor is in-network before booking — out-of-network visits can cost several times more.

- HMO plans require you to choose a designated PCP; PPO plans give you more flexibility but usually cost more per month.

- Most preventive care visits (annual physicals, screenings) are covered at no cost-sharing under the ACA, but this applies only to in-network providers.

- Bring your insurance card, a photo ID, and a list of current medications to your first appointment.

- Nurse practitioners (NPs) and physician assistants (PAs) are recognized as primary care providers by most insurers.

- Telehealth primary care visits are covered by most major insurers in 2026, though coverage details vary by plan.

- You can switch primary care doctors at any time — no reason required — though HMO members may need to update their PCP designation with their insurer.

- A multi-specialty practice lets your PCP refer you internally, cutting wait times for specialist care dramatically.

What Is a Primary Care Doctor and Why Do You Need One With Insurance?

A primary care doctor (PCP) is your main point of medical contact — the physician who handles routine checkups, manages chronic conditions, orders lab work, and refers you to specialists when needed. Having one on file with your insurance plan is often required for coverage and always beneficial for your long-term health.

Without a designated PCP, patients tend to rely on urgent care or emergency rooms for issues that could be handled at a fraction of the cost in a scheduled office visit. Research consistently shows that people with an established primary care relationship have better health outcomes, fewer hospitalizations, and lower overall healthcare costs (Agency for Healthcare Research and Quality, 2022).

If you’re wondering how to get a primary care doctor with insurance, the short answer is: use your insurer’s online provider directory, filter by specialty (family medicine or internal medicine), confirm the doctor accepts new patients, and book. The sections below walk through every step in detail.

Why it matters: Understanding the benefits of having a primary care physician goes beyond convenience — it’s one of the most evidence-backed ways to stay healthier over time.

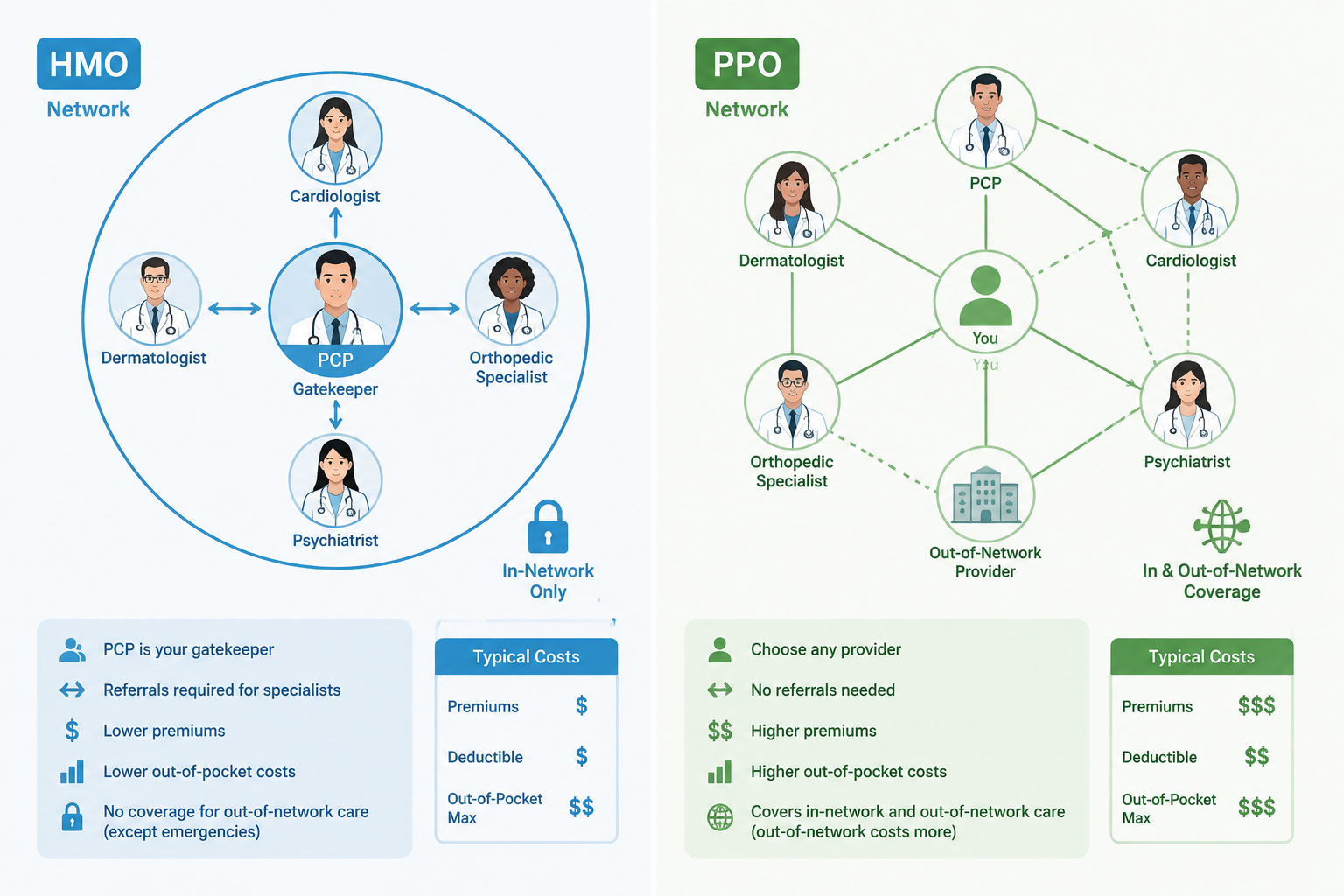

What’s the Difference Between HMO and PPO Insurance for Finding a Doctor?

HMO (Health Maintenance Organization) plans require you to select a designated in-network PCP who coordinates all your care, including specialist referrals. PPO (Preferred Provider Organization) plans let you see any doctor — in or out of network — without a referral, though in-network visits cost less.

Here’s a practical breakdown:

| Feature | HMO | PPO |

|---|---|---|

| PCP designation required? | Yes | No |

| Referral needed for specialists? | Usually yes | No |

| Out-of-network coverage? | Rarely | Yes (at higher cost) |

| Monthly premium | Lower | Higher |

| Best for… | People with a preferred local practice | Those who travel or want flexibility |

Choose HMO if you have a trusted local practice (like IDCC Health Services in Brooklyn) that handles most of your needs under one roof. Choose PPO if you see multiple specialists across different systems and don’t want referral paperwork.

For HMO members, selecting your PCP is not optional — it’s a required step when enrolling. Log into your insurance portal or call the member services number on your card to designate your PCP. This step is separate from booking an appointment.

How Do I Check If a Doctor Is in My Insurance Network?

The fastest way is to use your insurer’s online provider directory, which lets you search by doctor name, specialty, zip code, or practice name. Always call the doctor’s office directly to confirm — directories can be outdated by weeks or months.

Step-by-step:

- Go to your insurance company’s website and find “Find a Doctor” or “Provider Directory.”

- Enter your zip code and select “Primary Care,” “Family Medicine,” or “Internal Medicine.”

- Note the doctors listed as in-network for your specific plan (not just the insurer — the plan name matters).

- Call the practice directly and ask: “Do you accept [plan name] for [your insurer]? Are you accepting new patients?”

- Ask if the specific physician you want is in-network, not just the practice — individual doctors within a group can have different network statuses.

Common mistake: Assuming that because a hospital or clinic accepts your insurer, every doctor there does too. Always verify at the individual provider level.

IDCC Health Services accepts most major insurances including Aetna, Empire BlueCross BlueShield, Medicaid, Medicare, United Healthcare, Healthfirst, Fidelis Care, EmblemHealth, MetroPlus Health, and more. You can verify your coverage at idcchealth.org/insurance.php or call any of the three Brooklyn locations directly.

How Much Does a Primary Care Visit Cost With My Insurance?

With insurance, a primary care visit typically costs between $20 and $60 as a copay for in-network visits, though this varies widely by plan. Preventive visits (annual physicals, screenings) are usually covered at $0 cost-sharing under the Affordable Care Act when seen in-network.

Key cost factors:

- Copay: A flat fee per visit (e.g., $25 for primary care, $50 for specialists).

- Deductible: The amount you pay out-of-pocket before insurance kicks in. If you haven’t met your deductible, you may pay the full negotiated rate for the visit.

- Coinsurance: After your deductible, you may pay a percentage (e.g., 20%) of the visit cost.

- Out-of-pocket maximum: Once you hit this annual limit, insurance covers 100% of covered services.

Preventive vs. diagnostic visits: This distinction matters more than most patients realize. If you come in for your annual physical and your doctor addresses a new symptom during the same visit, that portion may be billed as a diagnostic visit — with different cost-sharing. Ask your doctor’s billing team before the visit if you’re unsure.

For a detailed look at what happens when you don’t have coverage, see how much a doctor check-up costs without insurance.

What Should I Look for When Choosing a Primary Care Physician?

The right primary care physician is one who is in-network, accepting new patients, speaks your language if needed, and practices in a location and style that fits your life. Clinical credentials matter, but so does the practical stuff: appointment availability, office hours, and whether specialists are accessible through the same practice.

Checklist for evaluating a PCP:

- Board certification in family medicine, internal medicine, or osteopathic medicine

- Accepting new patients (confirm by phone)

- In-network with your specific insurance plan

- Location and hours that work for your schedule

- Multilingual staff if English isn’t your first language

- Access to specialists through internal referrals (saves time and coordination effort)

- Same-day or walk-in availability for urgent needs

- Patient portal for messaging, lab results, and prescription refills

At IDCC Health Services, board-certified physicians including Dr. Inna Tovbina (Internal Medicine), Dr. Irina Pruchansky (Osteopathic Medicine & Family Practice), and Dr. Louis A. Carrera (Primary Care) see patients across three Brooklyn locations. The practice is an NCQA-Certified Patient-Centered Medical Home (PCMH) — a nationally recognized designation that signals coordinated, evidence-based care with measurable quality standards.

Related reading: Learn more about how to establish a primary care doctor easily and what that first visit actually involves.

What Documents Do I Need to See a Primary Care Doctor With Insurance?

Bring your insurance card, a government-issued photo ID, and a list of your current medications and dosages. If you’re transferring from another practice, request your medical records in advance.

Full document checklist for a new patient visit:

- Insurance card (front and back)

- Photo ID (driver’s license, passport, or state ID)

- List of current medications, including supplements and dosages

- List of known allergies

- Referral form (if required by your HMO plan)

- Medical records or summary from your previous doctor (optional but helpful)

- Any recent lab results or imaging reports

Edge case: If you’re on Medicaid or Medicare, bring your benefits card and any secondary insurance cards. Some practices also ask for your Social Security number for billing purposes — this is standard.

Can I Switch Primary Care Doctors If I’m Not Happy?

Yes. You can switch primary care doctors at any time and for any reason. There is no penalty for changing providers. HMO members need to update their PCP designation with their insurer (usually done online or by phone), which takes effect at the start of the next month in most plans.

Steps to switch:

- Find a new in-network PCP using your insurer’s directory.

- Confirm the new doctor is accepting new patients.

- If on an HMO, update your PCP designation through your insurer’s member portal or by calling member services.

- Request your medical records from your current doctor (you are legally entitled to them).

- Schedule a new patient appointment with the new practice.

Don’t feel obligated to stay with a doctor who dismisses your concerns. If you’ve experienced that, this guide on what to do when your doctor dismisses your pain offers practical next steps.

Is a Nurse Practitioner the Same as a Primary Care Doctor for Insurance?

For insurance purposes, nurse practitioners (NPs) and physician assistants (PAs) are recognized as primary care providers by most major insurers, including Medicare and Medicaid. They can serve as your designated PCP on most plans.

NPs like Marina Timoshenko, FNP and Tetyana Roytman, MS, FNP-BC at IDCC Health Services are board-certified family nurse practitioners who provide the full scope of primary care services: annual exams, chronic disease management, prescription writing, and specialist referrals.

Key distinction: Some HMO plans specifically require a physician (MD or DO) as the designated PCP. Check your plan documents or call member services to confirm whether an NP or PA qualifies as your PCP under your specific plan.

Are Telehealth Primary Care Doctors Covered by Insurance?

Most major insurers cover telehealth primary care visits in 2026, including Medicare, Medicaid, and commercial plans. Coverage expanded significantly after 2020 and has largely been maintained, though cost-sharing and eligible services vary by plan.

What telehealth typically covers:

- Routine follow-ups and medication management

- Mental health consultations

- Minor illness evaluation (cold, UTI, rash)

- Chronic condition check-ins (diabetes, hypertension)

What it usually does not cover via telehealth:

- Physical exams requiring hands-on assessment

- Procedures or injections

- Lab work or imaging (though orders can be sent electronically)

Practical tip: Confirm telehealth coverage with your insurer before your first virtual visit. Ask specifically whether the visit counts toward your deductible the same way an in-person visit does.

How Do I Find a New Doctor If I Just Moved?

If you’ve recently moved, start by calling your insurer’s member services line to get an updated list of in-network PCPs near your new address. You can also use your insurer’s online directory filtered by zip code.

Steps for new movers:

- Confirm your insurance plan is valid in your new state (some HMO plans are state-specific).

- Use the insurer’s provider directory with your new zip code.

- If your plan doesn’t have in-network providers nearby, you may need to switch plans during a Special Enrollment Period triggered by your move.

- Request medical records from your previous doctor before or shortly after moving.

Brooklyn-specific note: If you’ve moved to Brooklyn, IDCC Health Services has three convenient locations — at 445 Kings Highway, 201 Kings Highway, and 2846 Stillwell Avenue — and accepts most major insurance plans common to New York residents.

Also useful: Can you have a primary care doctor in another state? — this article breaks down the rules around cross-state primary care.

What If My Preferred Doctor Doesn’t Take My Insurance?

If your preferred doctor is out-of-network, you have four main options: pay out-of-pocket, ask if the practice offers a self-pay discount, switch to a PPO plan that covers out-of-network care, or ask the doctor if they plan to join your network in the future.

Option comparison:

- Pay out-of-pocket: Feasible for occasional visits; expensive for ongoing care. See what a doctor visit costs without insurance for benchmarks.

- Self-pay discount: Many practices offer reduced rates for uninsured or out-of-network patients who pay at time of service. Ask the billing department directly.

- Switch plans: If open enrollment is coming up, choose a plan that includes your preferred doctor.

- Ask about network joining: Physicians join new insurance networks periodically. It’s worth asking the front desk if they’re credentialing with your insurer.

Are Preventive Care Visits Covered by Most Insurance Plans?

Under the Affordable Care Act (ACA), most insurance plans are required to cover a defined set of preventive services at no cost-sharing when provided by an in-network provider. This includes annual wellness visits, blood pressure screening, cholesterol testing, certain cancer screenings, and recommended vaccinations.

Important caveats:

- “No cost-sharing” applies only to in-network providers.

- If your doctor addresses a new health concern during your preventive visit, that portion may be billed separately as a diagnostic service.

- Grandfathered health plans (those that existed before the ACA and haven’t changed significantly) may not be required to cover preventive services at no cost.

- Medicare has its own preventive benefit structure (Annual Wellness Visit, Welcome to Medicare visit) that differs from commercial plan rules.

Bottom line: Schedule your annual physical as a preventive visit, come prepared with any health concerns to discuss, and ask the billing team upfront how the visit will be coded if you plan to raise new symptoms.

How Long Does It Take to Get an Appointment With a New Primary Care Doctor?

National data suggests new patient appointments with primary care physicians average 20 to 26 days in major metro areas (Merritt Hawkins, 2022). However, practices with same-day availability — like IDCC Health Services — can dramatically shorten that wait.

Factors that affect wait time:

- Urban vs. suburban: Urban areas often have more providers but also more demand.

- Specialty: Family medicine and internal medicine tend to have shorter waits than some subspecialties.

- New patient vs. established patient: New patient slots are more limited at most practices.

- Time of year: January (post-insurance renewal) and September tend to be busiest.

Tip to get in faster: Call early in the week (Monday or Tuesday morning), ask specifically about cancellation lists, and consider whether a nurse practitioner or PA at the same practice can see you sooner.

Common Mistakes People Make When Choosing a Primary Care Physician

The most common mistake is choosing a doctor based on location alone without verifying network status or patient availability. Other frequent errors include:

- Not confirming the specific plan name — a doctor can accept Aetna but not your specific Aetna HMO plan.

- Skipping the new patient call — assuming online booking means the doctor is available.

- Ignoring office hours — a practice that closes at 4 PM on Fridays may not fit a working adult’s schedule.

- Not asking about specialist access — if you have a chronic condition, knowing whether your PCP can refer you internally to cardiology, neurology, or rheumatology matters.

- Choosing based on reviews alone — online ratings reflect patient satisfaction, not clinical quality. Board certification and PCMH status are more reliable quality signals.

- Forgetting to update your PCP on file with your HMO insurer after switching.

How to Get a Primary Care Doctor With Insurance: Step-by-Step

Here is the complete process, from insurance card to first appointment:

Step 1: Know your plan type. Is it an HMO, PPO, EPO, or HDHP? This determines whether you need a designated PCP and referrals.

Step 2: Access your insurer’s provider directory. Log in to your insurance portal or call member services. Filter by “Primary Care,” “Family Medicine,” or “Internal Medicine” and your zip code.

Step 3: Build a short list. Identify 3 to 5 in-network doctors or NPs with board certification and reasonable proximity.

Step 4: Call each practice. Confirm they accept your specific plan, are accepting new patients, and have appointment availability that works for your schedule.

Step 5: Book your new patient appointment. Provide your insurance information over the phone. Ask what documents to bring.

Step 6: Update your PCP designation (HMO only). Log into your insurance portal or call member services to designate your chosen doctor as your PCP.

Step 7: Prepare for your visit. Gather your insurance card, ID, medication list, and any relevant medical records.

Step 8: Attend your first appointment. Use this visit to establish your health baseline, discuss any concerns, and understand how referrals work within the practice.

FAQ: How to Get a Primary Care Doctor With Insurance

Can I see a specialist without a PCP referral?

It depends on your plan. PPO plans generally allow direct specialist access. HMO plans typically require a PCP referral first. Some EPO plans fall in between. Check your plan documents or call your insurer.

What if I don’t have a primary care doctor and need to see a specialist urgently?

Most specialists will see you without a referral for an initial consultation if you’re on a PPO or if the situation is urgent. For HMO members, call your insurer’s nurse line — they can often expedite a referral or direct you to urgent care.

Can I have two primary care doctors at the same time?

Your insurer will only recognize one designated PCP at a time, but you can technically see multiple providers. Learn more about whether you can have two primary care doctors simultaneously.

Does my primary care doctor need to be near where I live?

No, but proximity is practical. Choose a location you can realistically get to for routine and sick visits. IDCC Health Services has three Brooklyn locations to serve different neighborhoods.

Your Next Steps

Getting a primary care doctor with insurance doesn’t have to be complicated. The process comes down to four things: knowing your plan type, finding an in-network provider, confirming availability, and showing up prepared for that first visit.

In 2026, Brooklyn residents have strong options — and IDCC Health Services makes the process especially straightforward. With three convenient locations, same-day appointments, multilingual staff (English, Russian, Ukrainian, Georgian, and Spanish), and acceptance of most major insurance plans, IDCC removes most of the common barriers that delay people from establishing primary care.

Ready to get started?

- Call 445 Kings Highway (main location): (718) 715-0624 | Appointment line: +1-718-676-1710

- Call 2846 Stillwell Ave: (718) 715-0613 | Appointment line: +1-718-333-4111

- Call 201 Kings Highway: (718) 715-0629 | Appointment line: +1-718-484-7166

- Or visit idcchealth.org/contact.php to request an appointment online.

Don’t wait until you’re sick to establish care. A primary care relationship built before a health crisis is one of the most practical investments you can make in your long-term wellbeing.

Sources

- Lindquist, K. (2024). How Well Do You Know Your Insurance?. Narrative Medicine: Essays on Health and Care, 1(1), 6.

https://digitalcommons.providence.edu/cgi/viewcontent.cgi?article=1003&context=health

- Kyanko, K. A., Curry, L. A., Keene, D. E., Sutherland, R., Naik, K., & Busch, S. H. (2022). Does primary care fill the gap in access to specialty mental health care? A mixed methods study. Journal of General Internal Medicine, 37(7), 1641.